The 2026 Fosway 9-Grid Digital Learning Report highlights a market at an inflection point. On one side, AI is accelerating innovation at unprecedented speed. On the other, economic pressure is forcing organisations to scrutinise every rand, dollar, and pound spent on learning.

Two themes dominate: AI-driven transformation with limited differentiation, and a decisive shift toward value, outcomes, and Total Cost of Ownership (TCO). Together, they are redefining how L&D leaders should think about their digital learning strategy.

AI is everywhere. Differentiation is not

AI is now embedded across the digital learning lifecycle. From content creation and curation to coaching, simulations, and analytics. It is fundamentally reshaping how learning is designed, delivered, and experienced.

But here’s the paradox: while AI capability is expanding rapidly, true vendor differentiation is shrinking.

Most providers are building on similar large language models. As a result, features like AI-generated content, conversational learning, and role-play simulations are becoming standard rather than distinctive.

Why this matters

For buyers, it means the traditional approach of comparing feature sets is no longer sufficient. The real differentiators are shifting toward:

- Depth and quality of content

- Strength of underlying data and analytics

- Ability to drive measurable skills outcomes

- Consulting and service capability

In short, the question is no longer “What can the platform do?” but rather “What business problem can it solve?”

What organisations should do

Reframe vendor evaluation criteria: Move beyond feature comparisons and assess: (i) how well the solution integrates into your workflow, (ii) the quality and relevance of its data insights, (iii) its ability to support real skills application (not just content access)

Prioritise skills and performance over content volume

AI is enabling more immersive, practice-based learning, simulations, role plays, and adaptive feedback loops. These are far more aligned to capability building than passive content consumption.

Invest in internal capability: AI is lowering the barrier to content creation. Organisations can now produce high-quality, contextual learning experiences in-house, faster and cheaper than before.

How to put this into practice

- A financial services firm could use AI-powered simulations to train relationship managers on complex client conversations, replacing static compliance modules with dynamic, scenario-based practice.

- A retail organisation could deploy AI coaching tools for frontline staff, enabling continuous skills reinforcement rather than one-off training events.

- A consulting business could use generative AI to rapidly create bespoke learning journeys aligned to specific client engagements.

The key is to shift from content delivery to capability building.

Value over volume. The rise of TCO

If AI is reshaping supply, economic pressure is reshaping demand.

The report makes it clear: organisations are under increasing pressure to justify learning spend. Budgets are flat (or shrinking), buying cycles are longer, and procurement scrutiny is higher than ever.

This is driving a fundamental shift from “more content” to “more value.”

Why this matters

Historically, digital learning has been sold on scale: large content libraries, enterprise-wide licences, and consumption metrics.

That model is breaking down. Organisations are now asking:

- What measurable impact does this learning have?

- How does it improve performance or productivity?

- What is the true Total Cost of Ownership (TCO). Including implementation, integration, maintenance, and internal effort?

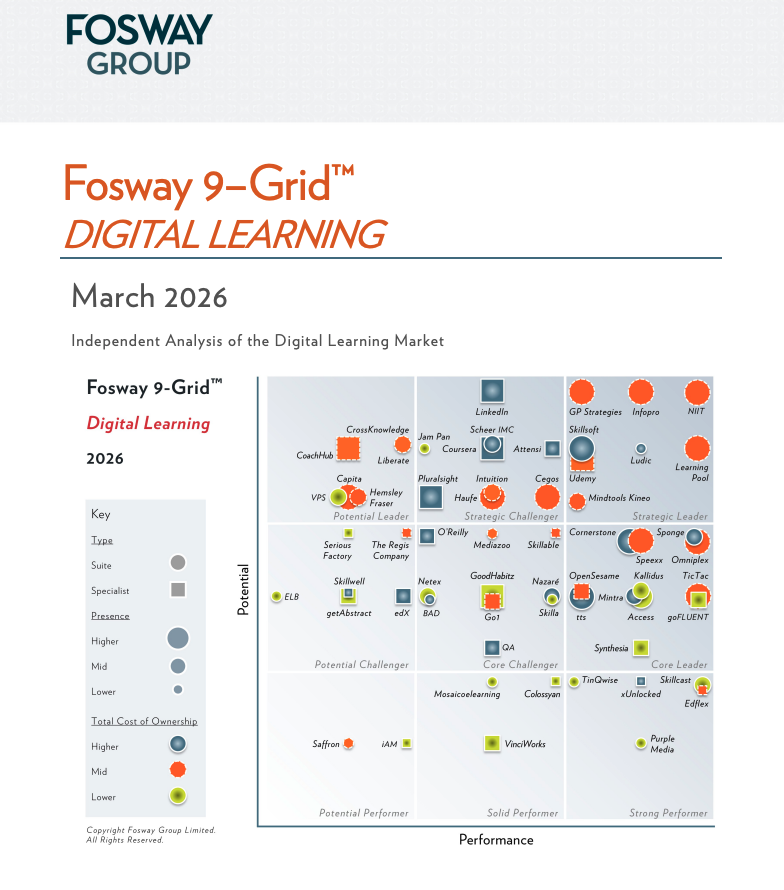

Critically, Fosway reinforces that the most expensive or most feature-rich solution is not always the best choice. Fit-for-purpose, cost-effective solutions are increasingly winning.

What organisations should do

Adopt a TCO mindset: Evaluate not just licence costs, but:

- Implementation and integration effort

- Internal resource requirements

- Ongoing maintenance and optimisation

- Opportunity cost of underutilised features

Consolidate the vendor landscape: Many organisations are reducing the number of suppliers they work with. Simplifying procurement, improving leverage, and reducing operational complexity.

Shift to outcome-based measurement: Move beyond completion rates and satisfaction scores. Focus on:

- Skills progression

- Behaviour change

- Business impact (e.g. sales performance, risk reduction)

How to put this into practice

- A bank could rationalise multiple content providers into a single strategic partner, reducing duplication and improving negotiating power.

- A telecoms company could link learning data to sales performance metrics, demonstrating ROI at a business level.

- A manufacturing firm could redesign compliance training using AI-driven personalisation, reducing time spent while improving retention and audit outcomes.

You can spend less, but achieve more.

What this means for South Africa and Southern Africa

For organisations in South Africa and the broader Southern African region, these trends are even more pronounced, and more urgent.

Why this matters locally

- Budget constraints are often tighter than in European or US markets

- Skills gaps are more acute, particularly in digital and leadership capabilities

- Infrastructure and access challenges require more flexible, scalable solutions

At the same time, the region has a unique opportunity to leapfrog legacy learning models and adopt more agile, AI-enabled approaches from the outset.

What organisations should prioritise

Cost-effective, high-impact solutions: TCO is critical in this market. Organisations should favour:

- Modular, scalable platforms

- Solutions that combine content, platform, and services

- Vendors with flexible pricing models

Skills-first strategies: With talent shortages in key areas, learning must be tightly aligned to business-critical skills. Not generic content libraries.

Blended and contextual learning: Given connectivity and access challenges, a mix of digital, mobile, and facilitated learning is essential.

How to put this into practice

- A South African bank could deploy AI-powered coaching for branch managers, improving leadership capability at scale without the cost of traditional executive coaching.

- A mining company could use simulation-based learning to train safety-critical behaviours, reducing risk while improving engagement.

- A pan-African business could build internal academies using AI-generated content, localising learning for different regions and languages at a fraction of traditional cost.

There is also a significant opportunity for local innovation. Combining global technology with deep contextual understanding of African markets.

Final thought

The 2026 Fosway 9-Grid makes one thing clear: digital learning is no longer about access to content. It is about driving measurable capability at the lowest sustainable cost.

AI is the catalyst. TCO is the filter. Value is the outcome.

For organisations willing to rethink their approach, this is less a challenge and more a moment of opportunity.

Written by Four and One Consulting.

Source: Fosway